Artificial Intelligence (AI) is more than just a buzzword and has experienced rapid growth over the last decade.

The consumer market is expected to grow from $54.4 billion in 2016 to $95.9 billion in 2021 at a compound annual growth rate of 12.0% from 2016 through 2021.

There may have been clear limitations in voice technology in the past, that have hindered rather than enhanced the customer experience. However, over the past 5 years, there have been radical breakthroughs in voice recognition.

What Will The #Voice #Tech #Revolution Mean For #Banking And #Fintech? #AI Click To TweetBrian Roemmele, CEO and founder of Payfinders has predicted:

“2017 will make 2016 – which was really the convergence point of artificial intelligence, machine learning, voice interactivity – look like slow motion”.

As voice assistants become more mainstream in vehicles, smart fridges in the home, mirroring the commonplace presence of digital assistants, such as Siri, Alexa and Google Home in mobile devices, – it’s inevitable that the voice biometrics will soon revolutionize the finance sector.

According to the researcher Gartner, AI bots will power 85% of customer service interactions by 2020.

Change is around the corner.

2. What developments are taking place in banking and fintech?

3. What is driving the disruption?

What Will The Voice Tech Revolution Mean For Banking And Fintech?

The rapid growth in the use of voice technologies is prominent throughout core industries. At this year’s Consumer Electronics Show (CES), 2017 was heralded to be “the year of voice recognition”. Voice recognition is being applied in many different forms in automotive, telecoms, insurance and banking industries and can range from biometric security to helpful chatbots.

1. Retail

Starbucks recently unveiled “My Starbucks Barista”, a conversational ordering system

2. Travel

Wynn Las Vegas and Amazon have announced its plan to equip all 4,748 hotel rooms at Wynn Las Vegas with Echo, Amazon’s hands-free voice-controlled speaker. The introduction of this technology into every guest room will be the first in its industry in the world, allowing guests of Wynn Las Vegas to control various hotel room features with a series of voice commands via Alexa, the brain behind Echo.

Steve Wynn, Chairman and CEO of Wynn Resorts commented:

“The ability to talk to your room is effortlessly convenient. In partnership with Amazon, becoming the first resort in the world in which guests can verbally control every aspect of lighting, temperature and the audio-visual components of a hotel room is yet another example of our leadership in the world of technology for the benefit of all of our guests.”

It will be interesting to see how customers and competitors respond to these changes. Will these features eventually filter into the mainstream?

3. Consumer Goods

At last month’s Consumer Electronic Show in Las Vegas, it was announced that Mastercard and Samsung, as well as Amazon and LG, have jointly developed new additions to their smart fridges, allowing users to order – and pay – for their groceries by voice.

4. Automotive

The automative biometric market is expected to grow steadily during the next four years

5. Insurance

Customers can now ask Amazon Alexa for over 300 insurance-related definitions

Voice Recognition technology is already gaining traction in the insurance industry. In early January, Fukoku Mutual Life decided to make 34 employees redundant in favor of artificial intelligence. The IBM Watson technology is capable of analyzing and interpreting an unstructured text, audio, and video data to calculate payouts. Around the same time, Aviva announced that it had created a new skill for Amazon Echo’s voice-activated intelligent assistant, Alexa. Customers can now ask Alexa for over 300 insurance-related definitions. Voice recognition will shape the future of insurance interactions.

Voice recognition technologies are allowing physicians, soldiers, and other users to achieve more by saving the time taken by written communications. The military sector, the industry’s largest investor, uses the technology to increase operational efficiency and for precision driving. North America remains the leading market in that sector, but Asia-Pacific countries are rapidly increasing their market shares.

1. Voice Application Platforms

Capital One is the first financial services company to sign up to the voice application platform Cortana. It has used existing voice technology to enable customers to manage their money efficiently through a hands-free, natural audible conversation with Cortana.

Cortana uses existing voice technology to enable customers to manage their money

CapOne and Amazon teamed up to put the Capital One “Skill” app on the Amazon Echo, allowing customers to access their bank accounts using their voice

Under a new pilot scheme, the company has revamped its voice recognition technology to allow customers to make transfers to existing payees by speaking to their iPhone SmartBank app. It is the first high street lender to offer the service and comes after the company launched its so-called “voice assistant banking” technology last year.

Santander customers will be able to make payments with their voice by talking to their smartphone app

“This pioneering technology has huge potential to become an integral part of the future banking experience, playing a transformational role in the industry and redefining how customers choose to manage their money.”

Santander first started to roll out the voice technology last March. Customers could give simple commands to the app, such as asking it to show historic transactions on their accounts.

Mr. Metzger said that updating the app to enable payments gives users “another channel of choice in how they wish to bank”. Lenders are investing heavily in technology to keep up with changing consumer trends, as more people shop, work, and watch television online. The rapid growth in digital technology has driven the decline in traditional bank branches, which lenders are shutting at a rapid pace.

2. Voice Biometrics In Security

Voice biometrics represents a giant step in the industry towards abolishing passwords and relying on more sophisticated security methods

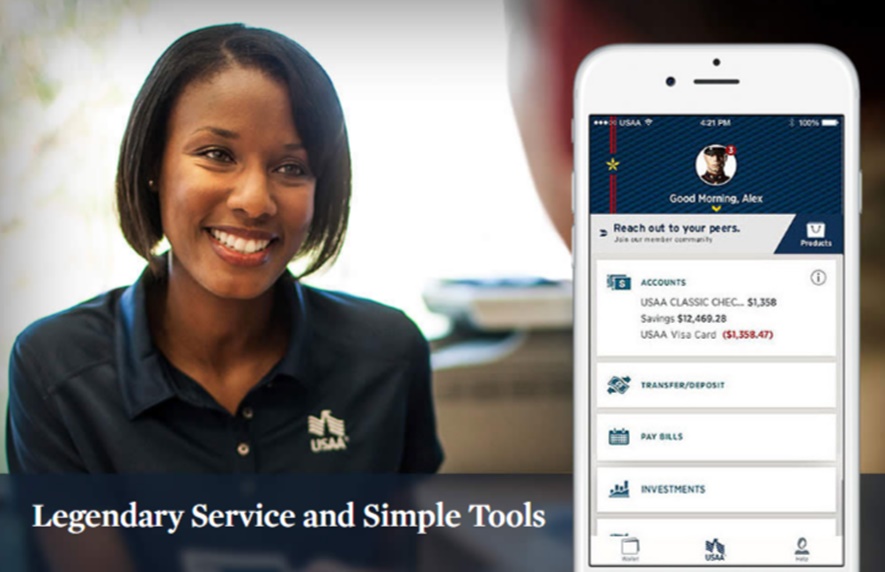

USAA facial recognition technology for banking app

USAA pioneered the adoption of facial recognition technology to mobile banking in February 2015 by introducing voice and face biometrics for customers to gain access to its app. Customers can activate the capability by going to the Quick Logon option within Settings and Profile in the mobile banking app. Face and voice recognition can then be selected before the customer electronically signs the terms and conditions.

To activate voice recognition, the customer must record the statement “My identity is secure because my voice is my passport. Verify me.” three times. This statement then needs to be said aloud when logging in.

Face registration is done by taking a picture before it is registered. During login, blinks are monitored for verification. This aspect helps to counter fraud, as a picture or video of a user would not be able to blink at the right moment.

The bank also offers fingerprint recognition to the biometric options available for logging in to its mobile banking app. Customers have the option to log in to the app using their preferred biometric method – face, voice, fingerprint or by entering a PIN. Apart from the biometric options for login security, the bank also uses device identification in the background, where an encrypted token is sent from the device to USAA which is then matched against the ID of the device registered at enrolment.

However, what are the risks of speech recognition technology – just how secure is it? Whilst banks claim that this new security feature is more secure than fingerprints, there are still serious concerns about the rapid increase in these modern technologies.

Banks seem to be developing voice biometrics-based on the assumption that everyone has a unique voice, but existing research has only been carried out on a small sample. Does everyone really have a unique voice signature? In addition, how might background noise interfere with the quality of voice recognition?

Think Silicon Valley meets Wall Street. Startups in financial technology – or fintech – are disrupting the industry by solving some of banking’s biggest issues, especially in local banking and consumer finance. As more customer interactions move online, the geographic advantage of local, high street banks is diminishing. After all, why would you visit a bank branch down the street to borrow money when you can shop for better interest rates from the comfort of your couch using peer-to-peer lending platforms like Lending Club, Prosper and SoFi?

Peer-to-peer lending platforms like Lending Club, Prosper and SoFi make it easy to borrow money

But convenience isn’t the only factor. According to Roji Oommen, managing director of financial services at CenturyLink, the biggest forces reshaping finance are:

1. Reduced Friction

Mint gives you an overall dashboard view of your financial health, pulling data from disparate sources

“This is also opening up opportunities to understand customers’ preferences, spending patterns via data mining and analytics,” Oommen said.

2. Robot Advisers

Automated investment services promise to take the pain and uncertainty out of investing by algorithmically constructing a portfolio, investing in ETFs, rebalancing, reinvesting dividends and even harvesting tax losses.

“You would just give your profile information and the algorithm will optimize investments for you,” according to Oommen.

3. New Business Models

As fintech entrepreneurs look to increase efficiencies, they are creating new business models. Crowdfunding companies such as Kickstarter have created a strong alternative to the venture-capital investment model. Several fintech companies like WorldRemit, TransferWise and Remitly are eyeing the global remittance market, which was estimated to exceed $600 billion in 2015, according to the World Bank’s Migration and Remittances Factbook. They are entering the market dominated by Western Union and MoneyGram with instant online and mobile-to-mobile transfer of money across borders at lower commissions.

Six major banks – Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Wells Fargo – have made investments in fintech companies since 2009, according to CB Insights. Several other banks are sponsoring incubators, accelerators, and hackathons to encourage tech experimentation. British bank Barclays, for instance, has set up an accelerator to provide advice, connections, and mentorship to fintech startups. It can be mutually beneficial for banks and startups to join up. For fintech companies, it makes more sense to use the incumbents’ infrastructure and investment dollars, especially in such a heavily regulated environment.

One thing is certain – disruption is good for the consumer. “We expect some shift in market share from one player to another, but the biggest change will be the way banks interact with customers,” Oommen said.

Banks are sponsoring incubators, accelerators and hackathons to encourage tech experimentation

However, a new technology is bound to need refinements before it can be a useful asset. The challenge for chatbots is to understand and show some human emotion. Emotion is a core driver of customer loyalty and chatbots may lack the EI to understand complex customer scenarios. When it comes to business the chatbot needs to be polite, intelligent and helpful without pretending to be human.

The future is bright for voice technologies which promise to enrich our experiences with digital devices. Our voices are going to bridge the gap between human-machine conversations and will be an integral part of daily transactions.

Even more game-changing is the use of biometric security – we have already seen how fingerprint identity has touched everyday life with our iPhones. It’s highly likely there will be a day when the customer’s most secure password is their voice.

As machine intelligence grows in its mastery of voice recognition and conversation, it encroaches upon a quality which sets us apart as human – the faculty of speech. As we rush to redefine what it means to be human, perhaps the more penetrating question is – does it even matter?

Does the customer care if she is talking online to a faceless chatbot rather than a faceless human?

We have entered an age where service is sovereign. Be it human, machine, or an intelligent combination of the two – it’s up to the industry to get it right.

The potential of voice biometrics has been recognized with the visually impaired, deaf or mute long before it gained traction in the mainstream:

“Able-bodied individuals gain convenience from voice-control technology, while the disability community gains the greatest reward of all: independence.” ~ Talk to the Machine: Voice Control Comes Into Its Own

Banking industry is moving to technologies that could one day see robots providing bespoke wealth advice and artificial intelligence answering customers’ questions

HSBC, which has closed the most branches of any UK bank recently, said last month that it had experienced a near 40% drop in the number of people using its branches. TSB, which announced an extra 29 closures last week, admitted that “some locations are very quiet, serving fewer than 200 people a week”. Meanwhile, Standard Chartered is moving heavily into radical new technologies that could one day see robots providing bespoke wealth advice and artificial intelligence answering customers’ questions.

Biometric authentication is “difficult to mimic and easy for people to use,” said Tom Trebilcock, senior vice president of digital at Pittsburgh-based PNC Bank, where customers with Apple iPhones equipped with Touch ID have the option of ditching passwords for fingerprints. “Looking out years from now, I expect the days for passwords are numbered,” he said.

However, whilst there is excitement and optimism in the fintech world about the development of this new technology it is important to remain circumspect.

Unscrupulous scammers are now using clever techniques, such as voice recording using Voice over Internet Protocol (VOIP) (also know as “voice phishing”), to gain access to personal information. This technology is likely to see a rise in scammers overcoming voice biometric security using your actual voice and information in payback to dupe banks.

According to the FBI, voice recognition is not perfect and only be used as one step in a multi-step security process.

Ultimately, banks will need to provide reassurance to customers that this new technology is secure in order to avoid a loss of consumer confidence in security.