Today’s economic climate is changing rapidly and so is the technology surrounding it.

This change can be seen clearly in the financial services industry which traditionally has been centralized by banks and other institutions; financial services today, however, are starting to become more and more decentralized.

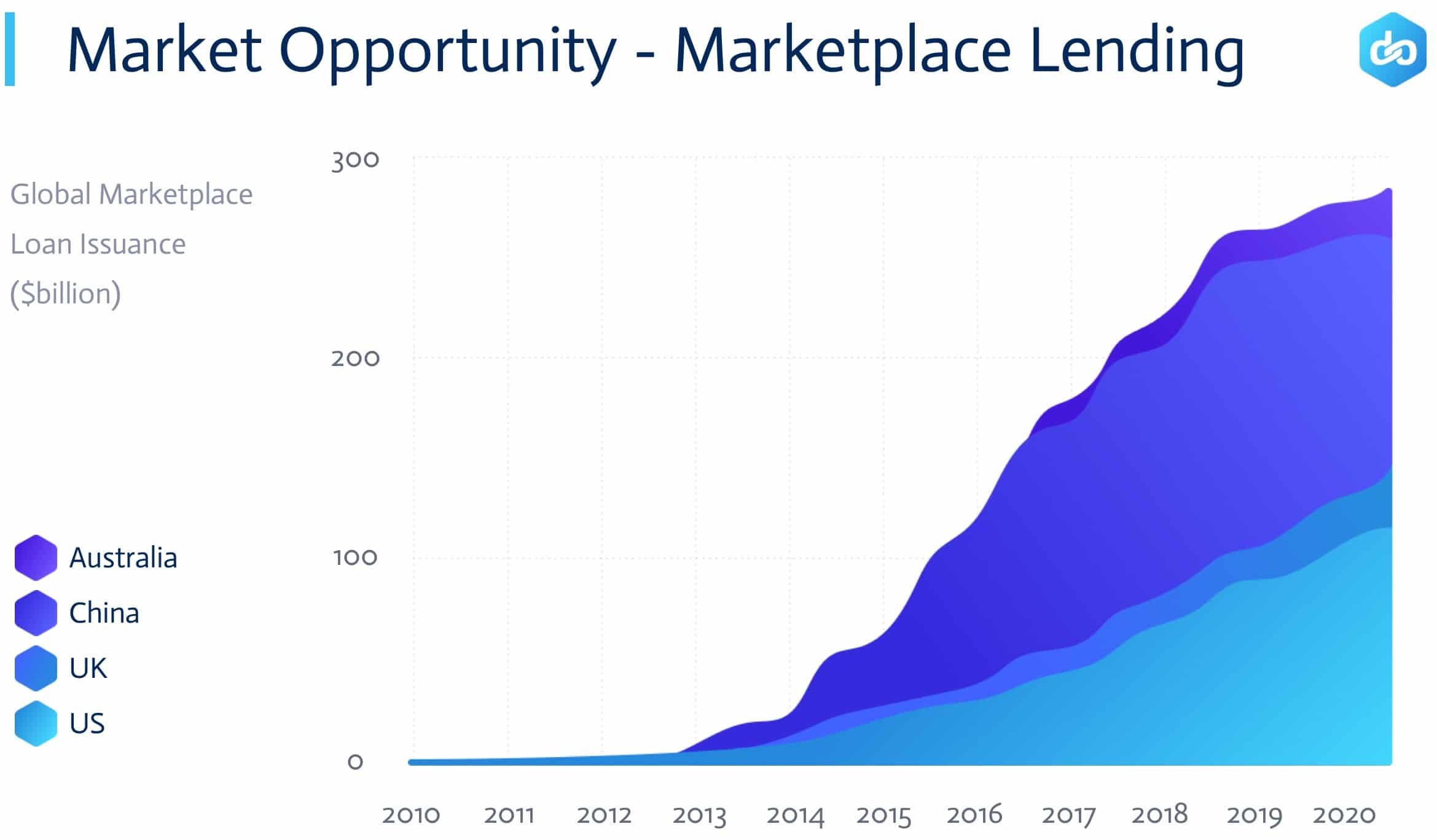

An example of this is in marketplace lending which are essentially online platforms that enable lenders to lend to retail and commercial borrowers.

Unlike how banks issue loans, marketplace lending do not take deposits or even lend capital themselves which means there are no risks to the marketplace financial-wise.

The business model of a marketplace lending platform depends solely on fees and commissions received from borrowers and lenders using the platform.

Peer-to-peer (P2P) lending, on the other hand, is the act of matching borrowers and lenders through online platforms.

With P2P lending, borrowers borrow at lower rates compared to banks and they also receive it more quickly (sometimes instantly). Lenders also revolve from individuals to institutional lenders which makes the system flexible.

There are, however, problems with the current state of marketplace lending.

Current P2P platforms are not really P2P because they need to have intermediaries like issuing banks or trust accounts for the system to work. This is a problem as intermediaries usually lack transparency and are also restricted geographically.

For instance, the annual interest of a loan in Brazil may be more than 50% while it is only 1% in Japan. So in a P2P platform, Brazilian users struggle because they have to extremely high premium rates for their loans while Japanese lenders cannot get high returns because of their low-interest rate.

Surprisingly, there is still no real solution for reducing interest rates for borrowers and increasing the rate of return for lenders in P2P lending platforms.

![]() Lendoit is a decentralized peer-to-peer lending marketplace platform that connects borrowers and lenders globally in a fast, easy, and extremely secure manner by using the blockchain and smart contracts.

Lendoit is a decentralized peer-to-peer lending marketplace platform that connects borrowers and lenders globally in a fast, easy, and extremely secure manner by using the blockchain and smart contracts.

With the blockchain, Lendoit is able to automate all of the processes required in P2P money lending without sacrificing anything. Instead, everything will be much cheaper and more efficient which is exactly the solution to problems of cross-border loans.

What makes the project strong is the team behind it.

Lendoit’s team is made up of many experienced individuals in the financial sector such as the founder and CEO himself, Ori Erez who will lead the fintech platform in achieving growth.

Lendoit also has an amazing advisory team to boot with some familiar names in the blockchain scene like Michael Terpin, the founder of BitAngels and CoinAgenda, Eddy Travia from the public listed company Coinsilium as well as Richard Titus who is an advisor to many influential blockchain startups.

Like traditional lending processes, the lending ecosystem in Lendoit consists of borrowers, lenders, collectors, and score providers.

First, borrowers must go through a quick application process which is essentially a KYC (Know Your Customer) process before they can begin using Lendoit. The process will also include some questions to understand the borrower more.

After a borrower’s request is submitted, the process of raising funds (also called a tender) begins.

What this tender does is to serve as a way to get the best offers in the shortest time possible.

The tenders work like a bidding structure in a reverse auction. The bidders, in this case, are lenders who want to loan their money; the winners of the auction are lenders who can give the lowest interest rates for their loans.

What happens when a borrower doesn’t pay his or her debt?

If a borrower cannot pay the loan or the interest amount, collectors in the Lendoit platform can buy the debt from a lender and minimize his or her losses.

Collectors are classified as authorized entities in a set of countries who also have the ability to take legal action against borrowers.

Once a borrower’s registration is submitted, score providers are used to giving scores to lenders who apply for the service. Score providers also provide verification services for identities in the platform.

Smart Loan Contract

The Smart Loan Contract works exactly how it sounds like.

Smart Loan Contracts contain the borrower’s details including his or her score as well as containing the conditions of loans and their respective tenders.

They also act as a trusted intermediary which holds and releases the funds for the borrower as well as interacting with the rest of the smart contracts on the platform (which we’ll cover later).

Smart Loan Contracts can also change the ownership of a loan and initiates a collectors’ tender in the case of a defaulted loan ( a loan that is not paid on time).

Smart Reputation Contract

The Smart Reputation Contract works similarly to credit score; in Lendoit, they act as the global score of an Ethereum address and can be utilized for other purposes other than credit transactions.

This contract gets updated whenever a lender lends money or when the borrower pays their debt or fails to repay the loan.

Smart Compensation Fund Contract

The Smart Compensation Fund contract protects lenders by covering their losses in the case of a borrower defaulting on a loan.

In each lending process, the Smart Loan Contract will send a portion of the workload to the Smart Compensation Fund Contract.

What this does is that when a loan default occurs, the lender will recover a part of their losses through the Smart Loan Contract.

Withdrawing funds

If the user wants to retrieve all or part of their Lendoit tokens in the channel that has not been sent to Lendoit, they can do so by withdrawing their funds.

The user then signs and releases a withdrawal request.

Making partial withdrawals are also allowed so users can keep the state channels open for future transactions within the Lendoit platform.

Smart Conversion Contract

The Smart Conversion Contract is responsible for converting currencies into the LOAN token when it comes to making transactions on the platform.

Aside from all of these wonderful features, Lendoit also offers a secondary market for lenders to trade loans. This tool allows lenders to instantly liquidate their funds anytime which is a huge advantage.

Lendoit Global Payments will launch a token for sale for the aptly named LOAN token.

Token name: LOAN

Token base: Ethereum (ERC-20 compliant)

Token supply: TBA

Token sale duration: December 13th, 2017

Token sale target: TBA

Token exchange rate: TBA